South Carolina Department of Consumer Affairs Letter

The South Carolina Department of Consumer Affairs sent out a letter in regard to South Carolina's motor vehicle dealers' laws and filing requirements. The letter is as seen below:

The South Carolina Department of Consumer Affairs (“the Department") is charged with enforcing several laws that may apply to your dealership. The purpose of this letter is to educate South Carolina motor vehicle dealers about the laws and filing requirements under the Department’s jurisdiction to ensure the dealership complies with them. For resources and guides available online, refer to the Department’s Guide for Auto Dealers (updated Fall 2023) found at consumer.sc.gov.

The Department’s Guide for Auto Dealers (updated Fall 2023) found at consumer.sc.gov. Advertising Motor Vehicle Sales and Leases rS.C. Code Ann. S 37-2-308. Federal Truth in Lending Act & Federal Consumer Leasing Act)

The Consumer Protection Code requires the Department to monitor compliance with the Federal Truth in Lending Act and the Federal Consumer Leasing Act for businesses throughout South Carolina. These acts prohibit unfair or deceptive advertising in any medium (television, internet, radio, etc.). Furthermore, S.C. Code Ann. § 37-2-308 provides various disclosure requirements for advertising motor vehicle sales and leases in South Carolina.

Motor vehicle dealers are ultimately responsible for the content and form of their ads. Advertising agencies and other third parties will be considered agents of the dealer and the dealer will be held accountable for any failure to comply with the law.

Consumer Credit Grantor Notification fS.C. Code Ann. S 37-6-201 to -204 and Reg. 28-8)

The requirement to file a Credit Grantor Notification applies to any person (includes any individual, organization, partnership, corporation, and association) who meets items 1,2, and 3:

1. Any person:

a. engaged in consumer credit sales, consumer leases, consumer loans, or consumer purchase agreements in South Carolina; OR

b. with an office or place of business in South Carolina who takes assignment of and undertakes direct collection of payments from or enforcement of rights against debtors arising from consumer credit sales, consumer leases, consumer loans, or consumer rental-purchase agreements.

2. Any person whose annual gross volume of business exceeds $150,000.

3. Any person who uses written agreements to extend consumer credit.

Notification must be filed with the Department on or before January 31st each year

Maximum Rate Schedules (S.C. Coilc Ann, SS 37-2-201, -305 and Reg. 28-70)

The requirement to tile and post a Maximum Rate Schedule applies to any creditor who wants to charge an Annual Percentage Rate (APR) in excess of 18% on consumer credit sales or consumer loans in South Carolina. This applies to both ”buy-here-pay-here” and ’‘indirect lending” business models. The Maximum Rate Schedule must be filed with the Department before the eredilor begins charging over 18% APR and on or before January 31 st each year.

Motor Vehicle Dealer Closing Fee tS.C. Code Ann. S 37-2-307) t*amcnded 5/16/2023*)

A closing fee is a fee for recovery of a motor vehicle dealer's actual costs for all administrative and financial work needed to transfer and deliver the motor vehicle to the consumer including, but not limited to, compliance with all state, federal, and lender requirements, preparation and retrieval of documents, protection of the private personal information of the consumer, records retention, and storage costs. Prior to charging a closing fee (sometimes referred to by other terms such as doc fee, doc prep fee, administrative fee, processing fee), a motor vehicle dealer must provide written notice to the Department of the maximum amount of a closing fee the dealer intends to charge.

If the maximum amount the dealer intends to charge is $225 or less:

- Complete and submit the Notice of Closing Fee Form and pay the registration fee;

- The proposed fee will automatically be considered reasonable; and

- The dealer can begin charging it after posting the Certificate issued by the Department.

If the maximum amount the dealer intends to charge is more than $225;

- Submit a completed Notice of Closing Fee Form and pay the registration fee;

- Submit a completed Addendum with supporting documentation';

- The proposed fee may be subject to review by the Department for reasonableness based on the information provided in the Addendum and supporting documentation; and

- The dealer can begin charging it after posting the Certificate issued by the Department.

The Department will notify the dealer within 15 days of receiving a complete application

(including the filing fee) that the Certificate has been issued or that the Department intends to conduct a review for reasonableness. In determining the reasonableness of a closing fee, the Department shall accept and allow all of the dealer’s actual costs and expenses including, but not limited to, employee compensation, infonnation processing, facilities costs, supplies, and materials associated with the following closing and delivery activities:

1. closing the motor vehicle sale or lease transaction, including any associated loan or lease and transferring title of the motor vehicle to the consumer;

2. delivering the motor vehicle to the consumer;

3. complying with all state, federal, and lender requirements;

4. preparing, storing, and retrieving transaction documents; and

5. protecting the private personal information of the consumer.

In determining the reasonableness of a closing fee, the Department may compare a particular dealer's costs only with other similarly situated dealers.

' Dealer costs must be calculated using generally accepted cost accounting principles for the preceding twelve month period.

The closing fee must be clearly and conspicuously disclosed with the advertised price of a motor vehicle, disclosed on the sale or lease contract, and displayed in a conspicuous location in the dealership. The dealer must file the closing fee with Department before it begins charging a closing fee but does not need to file again unless the dealer wants to change the fee (i.e., no annual renewal).

Repossession and Right to Cure Notice (S.C. Code Ann. SS 37-5-109, -IIP. -111)

Before repossessing a vehicle, a dealer (creditor) must inform a consumer of the default and give him or her 20 days from the date of issuing the Notice to cure the default. The Notice of Right to Cure must be sent after the consumer has been in default for more than 10 days for failure to make a required payment and has not voluntarily surrendered the collateral. A creditor gives notice to the consumer under this section when he delivers the notice to the consumer or mails the notice to him at his residence. A certified letter returned to the creditor does not satisfy the statute.

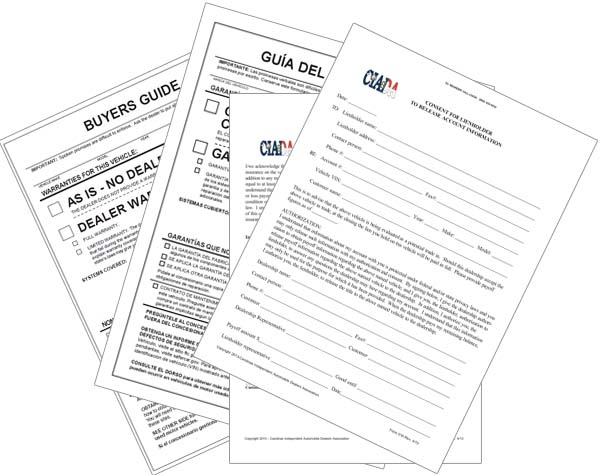

Used Car Rule and Buyers Guides (16 C.F.R, Part 455)

The Federal Trade Commission’s Used Car Rule requires motor vehicle dealers to display a window sticker, known as a ‘‘Buyers Guide,” on the used cars they offer for sale. The Buyers Guide discloses whether the dealer offers a warranty and, if so, its terms and conditions, including the duration of the coverage, the percentage of total repair costs the dealer will pay, and which vehicle systems the warranty covers.